Pet Health Insurance vs Human Health Insurance: Key Differences

As more pet owners seek peace of mind regarding veterinary care costs, pet health insurance has grown in popularity and now draws frequent comparisons to human health insurance. While both types of coverage are designed to reduce out-of-pocket expenses and support long-term health management, the similarities often end there. Understanding the key differences between pet health insurance and human health insurance in 2025 is essential for making informed decisions about financial planning, care accessibility, and policy value for both yourself and your furry companions. With healthcare innovation advancing on all fronts, the distinctions between these two systems highlight the unique ways each industry addresses risk, treatment, and preventive care.

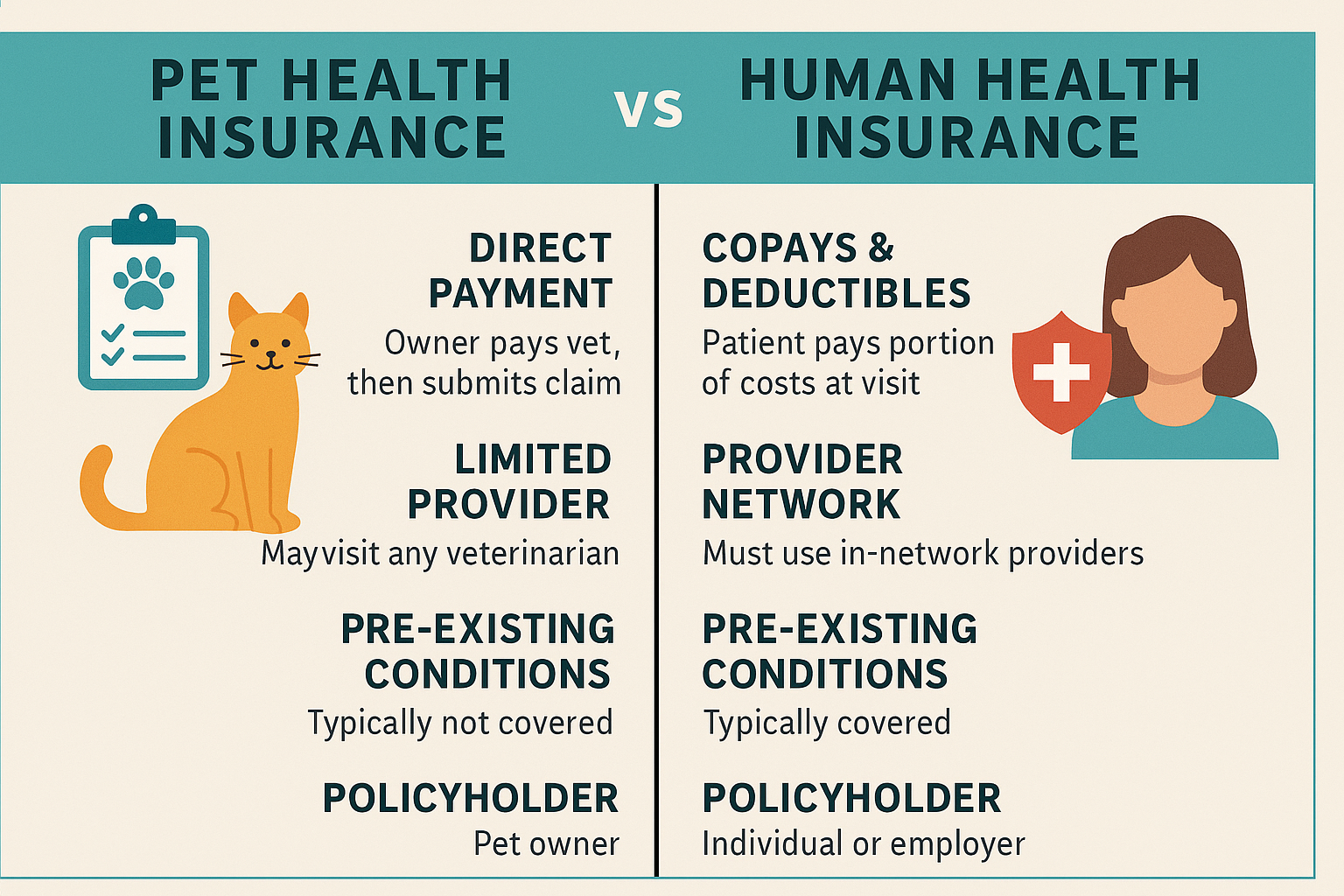

Unlike human health insurance, which is often employer-sponsored or subsidized through government programs like Medicare, Medicaid, or the Affordable Care Act (ACA), pet insurance is entirely voluntary and paid for by the pet owner. There are no mandates or subsidies for pet insurance, meaning the entire financial responsibility lies with the consumer. Premiums for pet insurance vary based on the animal’s breed, age, and medical history, and the scope of coverage is often narrower. Most pet insurance policies function on a reimbursement basis: the pet owner pays the veterinary bill out-of-pocket and then files a claim for partial reimbursement. In contrast, human health insurance typically involves direct billing with providers, co-payments, and in-network negotiations, reducing the immediate cost burden at the time of service.

Coverage scope is another major difference. Human health insurance plans are regulated to include a set of essential health benefits, such as maternity care, mental health services, and chronic disease management. These benefits are standardized under federal and state regulations. Pet insurance, however, is not federally regulated in the same way, leading to more variation between providers. Most standard pet policies cover accidents and illnesses but exclude preventive care unless added through a wellness plan. Routine exams, vaccinations, dental cleanings, and spay/neuter procedures often require additional premiums or are excluded entirely. Meanwhile, preventive care in human health insurance is widely covered due to its long-term cost-saving benefits and public health impact.

Pre-existing condition policies also differ significantly. Human health insurance providers, especially under the ACA, cannot deny coverage or charge higher premiums based on pre-existing conditions. This ensures equitable access to healthcare for individuals with chronic or past illnesses. On the other hand, pet insurance providers typically exclude pre-existing conditions, and many will not reimburse for any illness or injury that occurred before the policy was activated. This makes early enrollment in pet insurance critical for maximum benefit, while also reinforcing the need for careful plan comparison and review.

Another fundamental distinction is how care decisions are influenced. In human health insurance, medical choices are often driven by coverage limitations, referral requirements, or network restrictions. Patients may need pre-authorization for certain procedures, and there are strict billing codes tied to reimbursement. Pet insurance offers more freedom in provider choice, as most plans allow visits to any licensed veterinarian, including specialists. However, this freedom comes with the trade-off of higher out-of-pocket costs at the point of care and slower claim processing timelines. The administrative burden is generally lighter in pet insurance, but it places more responsibility on the pet owner to understand and manage claims.

In terms of cost, human health insurance tends to be more expensive due to the complexity of coverage and regulatory demands, yet it often provides broader protections and subsidies. Pet insurance, while more affordable in monthly premiums, offers less comprehensive coverage and often requires careful budgeting for unexpected costs. Deductibles, co-insurance percentages, and annual or lifetime caps are common features of both systems, but they tend to be more stringent and less standardized in pet insurance policies.

In conclusion, pet health insurance and human health insurance serve similar purposes—providing financial protection and access to essential care—but they operate under fundamentally different models. Understanding these differences is crucial for consumers who want to make responsible, cost-effective choices for their family and their pets. As healthcare systems evolve in 2025, both pet owners and individuals must remain informed about policy terms, benefits, and limitations to make the most of their coverage and ensure the well-being of everyone under their care, whether human or animal.